Article by Simon Dolan, Steven Hawkins, Chad Albrecht and Bonnie Richley

Originally published in The European Business Review

While most organizations have a code of conduct (or a code of ethics), many employees don’t care about, nor even recognize, their own company’s code of ethics. As pointed out by Liran and Dolan (2016)1, “There is a growing discrepancy between the values stated on the wall and values in action.” In the “Report to the Nations: 2020 Global Study on Occupational Fraud and Abuse”, the Association of Certified Fraud Examiners estimates that organizations lose approximately 5% of their revenue or $4.5 trillion globally to occupational fraud and abuse each year2. Furthermore, the European Anti-Fraud Office (OLAF) reports fraud of roughly €485 million to the EU budget in 2019 alone3. Clearly, there is a lack of ethics in both the private sector and in government. Research suggests that unethical behavior is not unique to a time or place and that unethical acts happen in organizations of all types and across all industries.

The Yale Center for Emotional Intelligence, in collaboration with the Faas Foundation, conducted a national survey of more than 14,500 employees across industries to better understand how Americans experience work. The sample represented the U.S. economy in its distribution of industries, sectors, and demographic diversity. While the majority of workers stated that they never, or almost never, experienced pressures from management (or direct supervisors) to act unethically, 11% sometimes experienced this pressure and 12% experienced this pressure often. In other words, 23%, or nearly one in four people, feel pressure to do things they know are wrong. In the research, the authors suggested that we need to find ways to alleviate the pressure to act unethically and prevent the fear of speaking up4. While there are many reasons that employees engage in unethical behavior, one reason is that employees want to find ways to benefit their organization. In the process, they often face a conflict between the desire to maximize self-interest and the desire to act ethically. Other reasons for engaging in unethical behavior may include: (1) Influence of supervisors and/or peers, (2) Actions consistent with Social Exchange Theory where employees feel underpaid and thus allow themselves to settle their lack of rewards by cheating and bypassing the organization’s ethical codes, (3) Productivity crisis and the perceived urgent need to do whatever it takes to contribute to the firm’s success.

Under which circumstances, are unethical acts most likely to occur?

While it is difficult to single out a specific industry where unethical acts are most likely to occur, research on ethics allows us to make some predictions. For example, companies with unrealistic revenue goals are more likely to pressure employees to cut corners to achieve short-term results. Such has been the case in social media, financial, retail, and multiple other industries, leading to frequent security and privacy violations. Furthermore, the desire to grow and control costs has consistently resulted in underfunding IT functions eliminating appropriate cybersecurity and customer data privacy policies and procedures. In some cases, governmental regulations have even been ignored to achieve business objectives. In the case of Volkswagen, for example, unrealistic market share goals trumped engineering integrity. As a result, under-resourced and difficult-to-achieve objectives led Volkswagen managers and engineers to commit fraud on a global scale for years.

Companies with unrealistic revenue goals are more likely to pressure employees to cut corners to achieve short-term results.

In the high tech industry, the market changes so quickly that there are additional pressures to behave unethically. For example, the speed with which artificial intelligence, autonomous vehicles, virtual reality, the internet of things, big data, and many other futuristic products are developed creates a vulnerability for many companies. This is further compounded by additional ethical issues such as artificial intelligence and other major technologies that could potentially impact society. Often, the need to beat the competition seems to override the responsibility to examine the ethical dilemmas they create leaving collateral damage. Such is the case with the immense speed and pressure to develop a vaccine for the COVID-19 pandemic. Due to a perceived lack of sufficient testing, and ignoring of internal controls on a scale rarely seen before, experts fear that a significant proportion of the population will be hesitant to get vaccinated when the first vaccines become available. In the eyes of many consumers, high tech equals high risk. And, if left unchecked, ethics will continue to be thought of as irrelevant creating significant consequences for both individuals, organizations, and societies.

Unethical acts are also more likely to occur in organizational units located in remote locations and with individuals who spend more time with people external to the organization, such as customers, vendors, contractors, and others in conflict of interest situations. “Out of sight” can often mean “out of control” when it comes to employee ethical behavior. Those who spend most of their time with individuals external to an organization may align loyalty and values elsewhere. They are frequently vulnerable to kickbacks, bribery, misappropriation of funds, and other ethical problems. This type of problem has recently shaken the royal family in Spain, where the King Emeritus received (while he was still the King), a bribery of about 75,000,000€ as gratitude for having Spanish companies build the high-speed train system in Saudi Arabia. This along with other ethical scandals, forced the King to abdicate his position as king and pass the honor on to his son. The full story and the ramifications of this scandal are still unfolding.

Unethical behavior is more likely when individuals or organizations rely on the law to define what is and is not ethical. We argue that the law is not sufficient and hence cannot cover every possible ethical dilemma. As a result, values become increasingly important. Shared values represent the cultural DNA of the firm. These core values should be posted publicly (on the web site and other documents of the firm) and be followed meticulously by all employees and stakeholders5. Failing to do so, may lead employees and others to act unethically.

Hopefully, most people would agree that the above behaviors are unethical even though they may not be illegal. A major contributor to the infamous Enron fraud was the fact that many of their “accounting games” did not violate any laws or specific accounting regulations but were still considered unethical.

What mechanisms are in place to promote or increase ethics?

Most organizations have a code of ethics or conduct that employees are trained on and expected to follow. Most companies also have various processes and hiring practices to filter out bad actors applying for positions. But in many instances, however, long-term employees are often the perpetrators of fraud. One bank, for example, found that the biggest percentages of fraud perpetrators were those that had been with the organization between 15-20 years, had worked themselves into positions of trust, and who had financial pressures in their lives.

Auditing is another mechanism that should promote and increase ethics. Auditing is a necessary process for the long-term health of any organization, whether large or small. Larger firms often employ their own internal auditing departments, while smaller firms often employ third-party auditing or shared services. Public companies are also required to have external audits of their financial statements. The auditing process is currently required to assess and correct the financial statements of an organization according to accounting standards and good internal control processes. While some firms will undergo operational audits to improve efficiency, they are typically not required. The only type of auditing required by law are financial statement audits and the related audit of internal controls over financial reporting for publicly traded companies. The primary focus on auditing is to detect errors in an organization’s financial statements or deficiencies in the organization’s internal controls over the financial reporting process. Detection can be one of the most important steps within the fraud prevention process, as most fraud schemes are not discovered for many months.

What mechanisms should be in place to promote or increase ethics?

The ACFE divides occupational fraud into three broad categories: (1) Asset Misappropriation – stealing or misusing an organization’s resources (86% of cases); (2) Financial Statement Fraud – intentionally misstating or omitting material information in an organization’s financial statements (10% of cases) of cases; and (3) Corruption – bribery, conflicts of interest, extortion etc. (4% of cases)6. External audits usually focus on only one type of fraud – financial statement fraud, leaving the majority of cases not subject to required audits. Asset misappropriation and corruption should also be included in the scope of combined audits or addressed with separate audits. Both asset misappropriation and corruption can significantly damage the financial health of an organization and often leave an audit trail that can be followed7.

In the wake of continuing major scandals within large corporations, calls from the public for corporate leadership to be held accountable are ever increasing.

In addition to financial performance, another category of performance indicators that could be used to assess companies business practices would be an ethics audit. Ethical business practices are more relevant than ever before in the business world. In the wake of continuing major scandals within large corporations, calls from the public for corporate leadership to be held accountable are ever increasing. Some companies have heard public opinion and are increasingly trying to conduct their business in an ethical manner. Ethical considerations also permeate the work of auditors, who often have to resolve ethical dilemmas that arise during the auditing process8. Given their experience and knowledge of company operations, financial statement auditors may be well positioned to also perform ethics audits as well.

Although organizational-led efforts to become more ethical are notable, no formal standards exist to determine what it means to be ethical. This paper calls for the establishment of formal standards of ethical business practices. Although the meaning of what is ethical may be subjective, objective standards for ethical principles based on situations could be developed during the ethics audit process. If a situation-based approach is used in addition to the establishment of principles, then the ethical audit would be built from a solid foundation. The standards should produce quantifiable and measurable results that will allow larger scale ethical issues to be measured and improved. If governments and other regulators care about ethics as much as financial performance, an “ethics audit” should be required by regulators. If an ethics audit is not required but organizations sincerely care about ethics, they should voluntarily undergo regular ethics audits and report the results of those ethics audits to stakeholders.

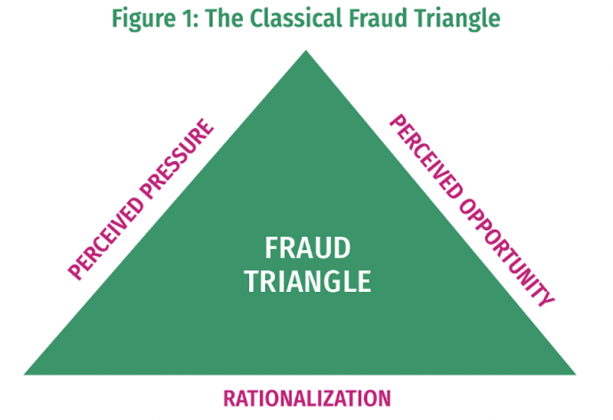

In addition to ethical standards, ethics auditing procedures and tools should be developed to assist companies and auditors in performing internal or external ethics audits. Albrecht et al (2017) suggests that the iconic fraud triangle could be applied more broadly to other types of ethical compromises, not just financial fraud. If this is the case, then the framework of the fraud triangle as expanded to the “Ethics Compromise Triangle” could be a useful tool to assess ethics of a company’s culture and identify strategies to improve9. Using the compromise triangle as a framework, more detailed and specific tools and audit procedures can be developed to increase the efficiency and value of ethics audits.

The fraud triangle is an old concept and has existed for over 30 years, It is probably the most iconic and fundamental fraud theory developed. It has thoroughly permeated the fraud, criminology, accounting, auditing, and marketing literature and has provided the basis for accounting policy decisions. It has been universally accepted in every setting where fraud is described or analyzed. The fraud triangle states that individuals are motivated to commit unethical behavior (i.e. fraud ) when three elements come together: (1) some kind of perceived pressure, (2) a perceived opportunity and (3) some way to rationalize the fraud as not being inconsistent with one’s values. The fraud triangle is depicted in Figure 1:

The purpose of the ethical audit is to assess and diagnose the ethics behind an organization’s actions and goals. An ethical audit would assess how well a company is living up to generally accepted ethical standards as well as its own ethical goals as an organization. In addition to building a more ethical foundation for the auditing process, the firms being audited will experience primary benefits to their organization. Firm leadership would be better able to determine if the ethical goals and guidelines set for the company are being met on an objective level. Leadership would have a valuable feedback tool to aid in the maintenance of a healthy ethical culture within an organization. The ethical audit will reveal if the firm has developed an ethical culture and will aid in the development of a better ethical culture in the future10. Various course corrections could be made if a firm’s current ethical goals are not met. The ethical audit also indicates the overall health of a firm. If a company engages in ethical practices, they are less likely to become a victim to fraud, and suffer from the financial losses associated with such activities.

An ethical audit would assess how well a company is living up to generally accepted ethical standards as well as its own ethical goals as an organization.

Much like the audit opinion firms receive for their financial statements, the creation of formal documentation that can certify a company as ethical would be beneficial for individual firms and the business community. Investor and consumer trust would increase, and the firm would be able to see a boost in its image within the business community. Firms have many benefits to gain when participating in an ethical audit. For an ethical audit to maintain the highest standards, the current approaches and attitudes towards auditing must change for the successful incorporation of a more ethical framework. Auditing practices should move from a rules-first approach to a principles-first approach, where ethical concerns are at the forefront of evaluative criteria11. An auditing approach that allows individuals to use an ethical framework will allow the implementation of an ethical audit. Additional transparency about the process will only help to foster a connection between a firm, its customers, and its shareholders.

Summary and conclusions

Regulations concerning the financial auditing process have increased over the years to ensure the system of financial auditing is better, more thorough, and more consistent. A series of recently passed laws in many countries seek to bring further transparency to the auditors and their processes. For example, following the lead of the EU, The United States of America also recently adopted standards requiring financial auditors to publicly disclose the name of each engagement partner12. The EU also passed a series of regulations called the 8th Company Law Directive, which required the establishment of an auditing committee for publicly traded companies to ensure the quality and transparency of financial reporting. Research has indicated that the effects of these laws on financial reporting quality have been positive13. If regulators and governments care about ethics similar attention should be given to ethical audits.

We call for laws and regulations that will require companies to undertake an ethical audit in a similar fashion to how these companies are required to undergo financial audits. Ethical audits will allow the discovery between what companies espouse and what they practice. Today, it is extremely difficult to know which companies are most ethical and which follow best business practices. Ethical audits will require companies to be held to a higher degree of transparency and responsibility. The establishment of new regulations will also increase the integrity of the ethical auditing process through the enforcement of formal standards.

Conducting an ethical audit can be crucial in the detection of any impropriety that would otherwise go unchecked. This can include uncovering unscrupulous or illegal activity within the firm, such as the unfair treatment of employees, customers, or suppliers. For example, the audit may reveal breaches of external regulations relating to excessive working hours or an unsafe working environment. The ethical audit is done not only to ensure that prohibited practices do not take place, but that behaviors advocated in a company’s code of conduct and within its written policies and procedures actually exist in practice. The value statements of a business should not be at odds with how its people behave. A dangerous precedent can be set by having corporate actions that are inconsistent with a company’s values.

The ethical audit is the next step in the evolution of a firm’s transparency to the public and a way to ensure that a company’s values are actionable and accountable. Too many scandals and fraud schemes have happened when large companies are trusted to manage everything themselves and there is no third-party verification. Although most of these scandals have been perpetrated by individuals, a system of regulation will enable perpetrators to be caught faster and the mere fact that ethical audits exist will deter many people from being dishonest in the first place. Ethical audits will result in fewer frauds and unethical acts and will help companies improve their public images. When ethics are at the forefront of business strategies and transactions, everyone profits from living in a more honest world where values are aligned with actions.

About the Authors

Prof. Simon Dolan is currently the president of the Global Future of Work foundation. Previously, he held several professorship positions in some of the leading management and business schools (Montreal and McGill, Boston and Colorado, ESSEC and HEC, and ESADE in Barcelona). He co-founded ISSWOV (The International Society for the Study of Work and Organizational Values). He is a prolific author with over 75 books published in multiple languages. He is also an entrepreneur that founded Gestions M.D.S. in the 1980s (in Canada) and currently is the honorary president of ZINQUO (in Spain). A high solicited speaker- Check him out at: www.simondolan.com or www.thinkingheads.com email: info@simondolan.com

Prof. Steven Hawkins is an assistant professor at Southern Utah University and received his PhD from the University of Tennessee. Stevens research focuses on fraud and ethics from an accounting perspective and has written multiple articles on the topic. Steven is currently a certified public accountant (CPA) and worked at Ernst and Young as an auditor for three years before pursuing a PhD. Email: stevenhawkins@suu.edu

Prof. Chad Albrecht is a Full Professor of Strategy & the Director of MBA Programs at Utah State University. At USU, Chad has received numerous awards including Researcher of the Year, Graduate Mentor of the Year and Undergraduate Research Mentor of the Year (3 times). Chad has also been a Robbins Research Finalist for his work on fraud prevention and detection. Chad has written six books and his fraud-related research has been quoted in the Times of London, In-Flight Magazine and various other news agencies. Email: chad@albrechtfamily.com

Dr. Bonnie Richley is the Chief Design and Innovation Officer for Interaction Science, a global consulting firm. She is a published author, keynote and motivational speaker. She has held numerous leadership positions in academia and in the public sector. Her work centers on high-impact engagement through individual and team coaching in organizations, adult learning, and transformational change. Email: b.richley@yahoo.com

References

- Liran, Avi and Dolan, Simon L. (2016) “Values, Values on the wall, Just do business and forget them all: Wells Fargo, Volkswagen and others in the hall” The European Business Review https://www.europeanbusinessreview.com/values-values-on-the-wall-just-do-business-and-forget-them-all-wells-fargo-volkswagen-and-others-in-the-hall/

- Association of Certified Fraud Examiners. (2020). Report to the Nations: 2020 Global Study On Occupational Fraud and Abuse. https://www.acfe.com/report-to-the-nations/2020/.

- https://ec.europa.eu/anti-fraud/investigations/fraud-figures_en

- Source: Zorana Ivcevic , Jochen I. Menges and Anna Miller: How Common Is Unethical Behavior in U.S. Organizations? Harvard Business Review, March 20, 2020 (https://hbr.org/2020/03/how-common-is-unethical-behavior-in-u-s-organizations)

- Dolan, S.L. (2020) The Secrets of Coaching and Leading by Values. London-NY Routledge.

- Association of Certified Fraud Examiners. (2020). Report to the Nations: 2020 Global Study On Occupational Fraud and Abuse. https://www.acfe.com/report-to-the-nations/2020/.

- Espinosa-Pike, M. and Barrainkua, I. (2016). “An exploratory study of the pressures and ethical dilemmas in the audit conflict.” Revista de Contabilidad. Vol. 19,Issue 1. https://doi.org/10.1016/j.rcsar.2014.10.001.

- Jeppesen, K. (2019). “The role of auditing in the fight against corruption.” The British Accounting Review. Vol. 15, issue 5. https://doi.org/10.1016/j.bar.2018.06.001.

- Albrecht, Chad; Albrecht, Conan; Hawkins, Steven (2017) “Is there an Ethics Compromise Triangle?” Internal Auditing, Vol. 32:4. pp. 5-20

- Semradova, I. and Hubackova, S. (2015). “Observations on the development of ethical culture.” Procedia – Social and Behavioral Sciences. Vol. 182. https://doi.org/10.1016/j.sbspro.2015.04.737.

- Satava, D., Caldwell C., and Richards, L. (2006). “Ethics and auditing culture: Rethinking the foundation of accounting and auditing.” Journal of Business Ethics. Vol. 64, no. 3. https://www.jstor.org/stable/25123749.

- Reid, C.D., and Youngman, J.F. (2017). “New audit partner identification rules may offer opportunities and benefits.” Business Horizons. Vol. 60, issue 4. https://doi.org/10.1016/j.bushor.2017.03.008.

- Bajra, U. and Cadez, S. (2018). “Audit committees and financial reporting quality: The 8th EU Company Law Directive perspective.” Economic Systems. Vol. 42, Issue 1. https://doi.org/10.1016/j.ecosys.2017.03.002.